7 Simple Steps to Regain Financial Stability and Get Your Life Back on Track

Life is full of unexpected twists and turns, but when it comes to your financial stability, it can be hard to know where to start to get back on track.

Being in debt can be overwhelming, but it doesn’t have to stay that way. With the right steps and a bit of dedication, you can regain financial stability and get your life back on track.

In this article, you’ll learn 7 simple steps to gain financial stability, from creating a budget and tracking your spending, to understanding your debt and creating an emergency fund.

With the right guidance and a bit of commitment, you can take control of your finances and get your life back on track.

Understand Your Current Financial Situation

Before you take any action, it’s important to understand your current financial situation.

You need to start by collecting a few numbers

- How much debt do you have?

- How much money are you bringing in a month?

- How much money are you spending a month?

- What’s your net worth? Everything you own minus what you owe

- What’s your financial freedom number? 25 x your annual spend.

First, you need to know how much debt you’re currently in.

Understanding what type of debt you have, how long you’ve had it, and how much you owe, will help you take the steps needed to regain financial stability.

Understanding your current financial situation will also help you figure out how you got into debt in the first place. This can help you avoid the same mistakes in the future.

Next, you need to look at your monthly income and expenses. This will help you get a better idea of how much you can afford to put towards your debts and everyday expenses. This is a critical part of regaining financial stability.

A budget can help you track your income and expenses and make sure you’re staying on track. Understanding your current financial situation will help you take the steps towards regaining financial stability.

Finally figuring out your net worth and financial freedom numbers will help you understand where you stand right now and where you may want to try and get to, to regain your financial stability in the long term.

Create a Budget and Track Your Spending

Creating a budget and tracking your spending is the key to getting on top of your money.

This will help you figure out how much money you’re making every month and how much you’re spending.

It’s important to know where your money is going because it can help you make better financial decisions.

A budget is a plan for how you’re going to spend your money. It can help you prioritize what’s important in your life and decide how to best use your money.

Budgeting doesn’t have to be complicated. You could try the Kakeibo method which just involves using 2 books.

There are many free tools you can use to track your spending and create a simple budget.

Be sure to choose a tool that is easy to use, so you’ll actually stick to your budget.

You can find many different types of budgeting apps online.

Make a Plan to Pay Off Your Debt

Once you have a clear understanding of your current financial situation and you know where your debt is at, you can make a plan to pay off your debt.

Make sure you have a plan for every type of debt you have, including monthly payment amounts, interest rates, and how long it will take you to pay it off.

This will help you stay accountable and on track.

Additionally, it’s important to be honest with yourself when creating a budget and making plans to pay off your debt.

If you’re spending too much and don’t have a plan in place, you’ll never get out of debt.

Make sure your plans to pay off your debt fit into your budget and don’t put too much pressure on yourself.

While it’s great to have ambitious goals to pay off your debt, you also want to make sure you don’t forget to have fun and stay motivated along the way.

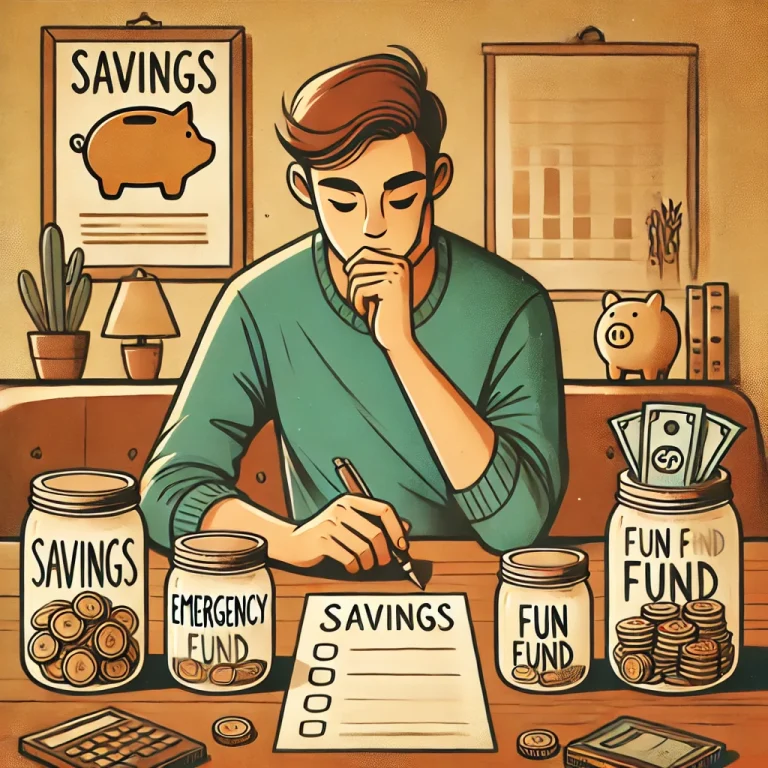

Create an Emergency Fund

An emergency fund can help you stay financially stable when unexpected things happen, like a car breakdown or health scare.

It’s important to have a financial safety net in place to help you stay on track when the unexpected happens.

Keep in mind that an emergency fund is for real emergencies, not just cash flow difficulties.

An emergency fund can help you stay out of debt and maintain your financial stability.

But how much should you save?

Experts recommend saving at least three months’ worth of your essential living expenses. This means saving enough money to cover your rent, groceries, transportation, and utility bills for three months if you lose your job or encounter an unexpected health expense.

Automate your finances

Next, you can take steps to automate your finances.

Automating your payments, saving, and investing can help you save time and energy and stay focused on other financial goals.

It can also help you avoid late payment fees and stay on track when it comes to paying your bills on time.

This can help you avoid having to manually pay your bills each month and make sure you’re on track.

Automating means you can remove the weakest link in your financial system – YOU – from some of the most important tasks i.e. getting it done.

Consider Ways to Increase Your Income

If you’re in a lot of debt and don’t have enough to pay it off quickly, you may want to consider ways to increase your income.

This can help you speed up the process of getting out of debt and gaining financial stability.

You can look for a second job or consider starting a side hustle to make some extra cash.

Could you use your skills and experience to coach or teach others in what you know through a blog, youtube or face-to-face ways?

You can also consider getting a new job at a company you believe in and making a career change if it’s something you’re passionate about.

Finding a job you love or are passionate about can also help you avoid feeling bored and unfulfilled and make it easier to get out of debt and stay financially stable.

Find Ways to Reduce Stress and Stay Motivated

Finally, you may want to find ways to reduce stress and stay motivated.

This can help you stay on track when it comes to paying off your debt and regaining financial stability. Y

ou can find ways to reduce stress, such as meditating, exercising, or spending time with friends and loved ones. You can also find ways to stay motivated, such as joining a support group or reading self-help books.

Whatever you do, don’t get discouraged.

Getting out of debt takes time and can be frustrating, but with the right steps and a bit of dedication, you can regain financial stability and get your life back on track.

FAQ: The importance of financial-stability

What is the meaning of financial stability?

Financial stability means being able to meet your current day-to-day expenses while also being able to plan and save for the future. Being able to deal with bumps in the road without going into debt. Being financially comfortable and able to plan for a bright future.

What determines financial stability?

Financial stability is determined by your ability to meet current expenses, and have savings to deal with expected and unexpected costs whilst also being able to build for the future. You have the ability to cope with and plan for the short, medium, and long term.

Why is financial stability so important?

Financial stability is so important because without it you will likely be living paycheck to paycheck or just one slip away from financial ruin and poverty. You need to be financially stable to cope with the ups and downs of life and be able to cope with them all.

Creating your own GAME Plan

If you would like to find out more about making a life and financial plan, figuring out how to reach your favourite future, and creating the assets and income you need to pay for this get in touch below or set up a call with us.